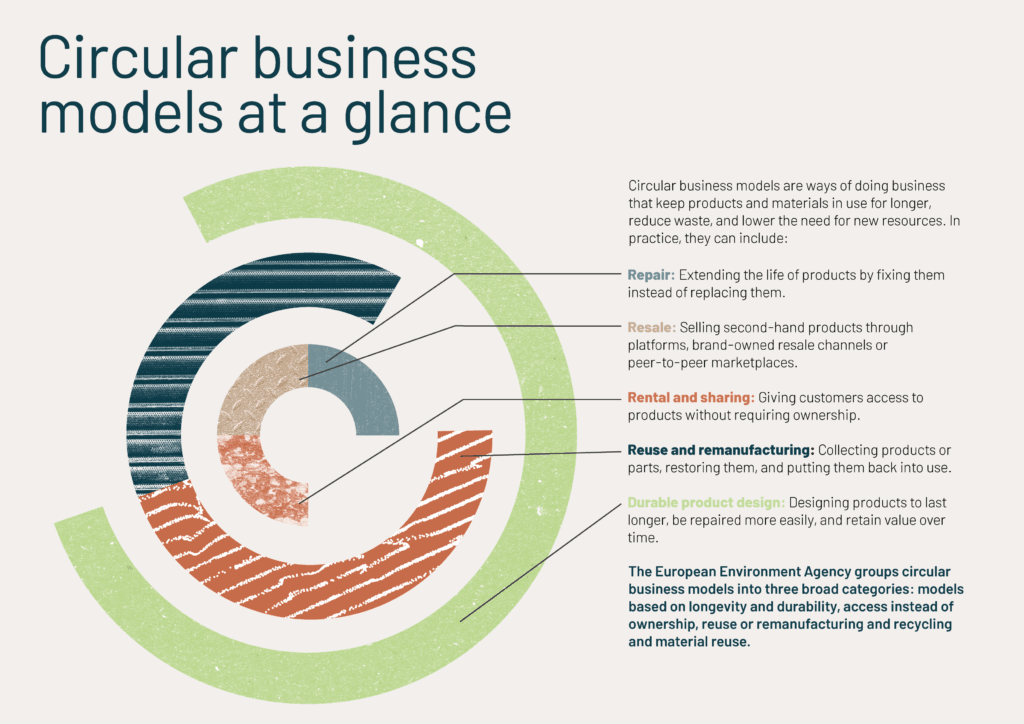

Circular business models in the EU are no longer a niche topic. Repair, resale, rental and reuse are attracting growing attention from policymakers, companies and investors. The reason is simple: these models can help reduce waste and keep products in use for longer. Circular business models also create a new resilient revenue stream and a new way of interacting with customers – it is not only about reducing waste. But they also face a difficult reality. In many sectors, it is still easier and cheaper to sell new products than to repair, resell or reuse existing ones.

Circular business models are gaining ground — but scale is still hard

In fashion, the shift is already visible. Anecdotally, shopping for vintage fashion/second-hand clothing has never been more popular. According to figures from the Ellen MacArthur Foundation, the worldwide second-hand market grew by 13% in 2025, making up around 10% of all clothing spend (from ThredUp’s 2026 Resale Report). The circular fashion market is expected to reach up to USD 393 billion by 2030. The Foundation also points to early results from The New Bottom Line report, where participating brands and retailers are reportedly growing revenue from resale, rental, repair and remaking four times faster than broader revenue in the participating part of their business. Vinted is now described as the biggest retailer by volume in France and the third largest by revenue in the UK.

But growth does not mean the business case is straightforward. Many circular models still operate in a system built around linear sales: make, sell, discard, replace. The policy question is therefore not only how to encourage circularity, it is also about how the EU can create the conditions to make circular business models easier to operate, finance and scale.

The growth of resale and repair/reuse shows that circular business models can attract demand. But demand alone will not solve the structural barriers. If the EU wants these models to move beyond early growth, policy needs to address the economics behind them: labour intensity, infrastructure, access to used products, demand signals and finance.

Why circular models are still hard to scale

Circular business models are still hard to operate profitably at scale. This is because they are competing in an economy still built for linear sales. Repair, refurbishment, remanufacturing, sorting, quality assessment and take-back schemes often require more labour than linear production models. They can also be difficult to automate or standardise. Circular businesses need reliable flows of used products in good enough condition to be repaired, resold or reused. When those inflows are inconsistent, it becomes harder to plan, invest and grow.

As Valérie Boiten, Senior Policy Officer at the Ellen McArthur Foundation explained for this blog, even where the resale market is growing, many business models struggle to become profitable because sorting, cleaning and repairing remain labour-intensive. “In the current system, it is cheaper to make new clothes than to invest in the people and infrastructure needed to deliver resale and repair services….” , she pointed out.

These activities do not become much cheaper simply because volumes increase. In contrast, linear production often benefits from economies of scale: producing more can reduce the cost per unit: “Sorting, cleaning, and repairing 100 items of used clothing takes 100 times the effort of sorting, cleaning, and repairing one. In the linear economy on the other hand, increasing production leads to lower costs per unit produced, which is essential to price competitiveness,” – added Valérie Boiten, of the Ellen McArthur Foundation.

This is the structural disadvantage at the heart of the debate. Circular businesses are being asked to compete in a market that was not designed for them.

The policy question: can Europe make the business case work?

Several policy tools are now being discussed to help circular business models scale, in particular: taxation. Reduced VAT rates for repair services already exist in some Member States under the EU VAT framework. The Netherlands, Ireland and Sweden have used reduced VAT rates for selected repair services, while France has introduced a repair bonus scheme that allows a fixed amount to be deducted directly from the consumer’s bill when a product is repaired by a certified repairer. and more than 69 businesses agree with this agreement, having signed a business statement by the Ellen MacArthur Foundation

Industry voices are now calling for this logic to go further. Clara Cherblanc, Head of Advocacy and Public Affairs at the Fédération de la Mode Circulaire, argues that “a reduced VAT rate for circular activities would directly improve the business case for companies investing in repair, reuse, rental, upcycling and resale infrastructures.” She also points to the need for public policy to de-risk investment in circular value chains and create a more level playing field between models that extend product lifetimes and those based on the continuous production and sale of new products.

The modelling behind the Ellen MacArthur Foundation’s new report The New Bottom Line, also backs up this argument. It suggests that three policy levers — reduced VAT on second-hand items and repair services, lower labour taxes for resale and repair jobs, and ambitious Extended Producer Responsibility implementation to fund collection, sorting, resale and repair infrastructure — could raise gross profit margins to up to 55% for resale and 41% for repair across the EU. This suggests that circular models are not inherently uncompetitive. Rather, their competitiveness depends heavily on the policy and market conditions around them. And as Valérie Boiten, of the Ellen McArthur Foundation points out: these kinds of incentives can “enhance the economic competitiveness of resale and repair, and help to rebalance the economics of fashion in favour of circular business models.” And more than 69 businesses agree with this, having signed a business statement by the Ellen MacArthur Foundation

Public procurement can help create demand

Public authorities buy large volumes of goods and services. If procurement rules reward durability, repairability, reuse and lifecycle value, they can create demand for circular products and services.

More streamlined and harmonised EU-wide circular procurement approaches could help scale demand and give industry greater certainty to invest in circular business models. As Francesca Fina from Ohana Public Affairs puts it: “Today, contracting authorities often prioritise upfront costs over lifecycle value — disadvantaging circular products and services. With the new Public Procurement Act expected later this year, there is a clear opportunity to raise ambition. However, significant uncertainty remains on whether the Commission will deliver truly impactful measures. Moving beyond lowest-price logic, by better accounting for lifecycle costs and circular features like durability, repairability and reuse, would help create a more level playing field for circular solutions.”

Can Extended Producer Responsibility carry all these expectations?

Extended Producer Responsibility (EPR) is already central to circular economy policy. It can help fund collection, sorting and treatment systems, and it can create incentives for better product design. But there is a risk in expecting EPR to solve everything. Stakeholders are already raising concerns about how EPR funds are distributed. And there is growing competition between different actors seeking access to limited funds, including sorters, recyclers and circular service providers. Last summer, for example, in France, textile sorters protested over the low compensation they received from Refashion, the French Producer Responsibility Organisation (PRO), for their textile sorting activities.

This raises a question: can EPR schemes support collection, sorting, recycling infrastructure, eco-modulation, repair, resale and circular business model innovation all at once? That does not mean EPR is the wrong tool. But EPR should be part of a broader policy mix, alongside taxation, public procurement, repair incentives and targeted finance.

The next test for EU circular economy policy

In order to truly achieve a circular economy, enabling conditions need to be created through both policy and investment. The full business case for circular business models needs to be examined: operating costs, labour intensity, access to used products, infrastructure, demand and investment certainty.

Finance is, of course, critical. According to a European Investment Bank study, the EU faces an estimated €82 billion annual investment gap to meet its circular economy objectives by 2040. Part of that gap relates to scaling circular business models, which require upfront investment in collection, sorting, repair, logistics, digital systems and new service models. A resale or repair model may need warehouses, trained staff, sorting systems, quality checks, traceability tools, and reverse logistics before it can reach scale.

The EIB has pointed to several ways to close this gap, including wider use of risk-sharing financial instruments, more grant funding, dedicated venture capital for circular economy companies, and tailored credit lines supported by clear circular economy criteria.

The EU Circular Economy Act: can it rise to the challenge?

Public policy can help create the market conditions, such as levelling the playing field between circular business models and traditional models by reducing VAT on them. But, given the political sensitivity of taxation (and the strong reluctance of Member States to agree on this), it seems unlikely that the Commission will propose a VAT reduction.

It’s clear that circular business models are gaining ground. Is the European Commission ready to respond to wide-ranging calls from stakeholders and translate them into concrete measures under the Circular Economy Act (expected to be presented in Q3 2026, after the summer) to make CBMs easier to finance, easier to operate and easier to scale? Policy makers need to take a broad look at the different tools available to them: Could public procurement criteria provide stronger market signals in support of circular services? And what role might there be for financial tools, such as targeted loans, EU funding, or blended finance mechanisms?

It is only if Europe builds the policy and finance conditions that allow circular business models to compete with the linear alternatives they are seeking to replace that they will be able to truly scale.

Related to this article, also see:

Waste Framework Directive Revision: the Impacts on Textiles & the Questions Left Unanswered

The EU Circular Economy Act Explained: Context, Content and Next Steps

Beyond Textiles: A Roadmap of EU Circular Economy Policies Across Sectors

At Ohana, we support companies in monitoring and engaging with EU policy, and in preparing for the implementation of EU legislation in a fast-moving environment. If you would like to discuss what is happening in Brussels and what it means for your organisation in practice, feel free to get in touch.